Conventional mortgages are the most popular form of home financing for buyers in the United States. However, it may not always be clear how these loans differ from other loans, such as those provided by government agencies. To help you gain a better understanding of conventional loan basics, here is a quick guide with further information:

When obtaining conventional financing, your lender will examine your financial situation. The loan officer may request information including your credit score, income statements and debt to income ratios.

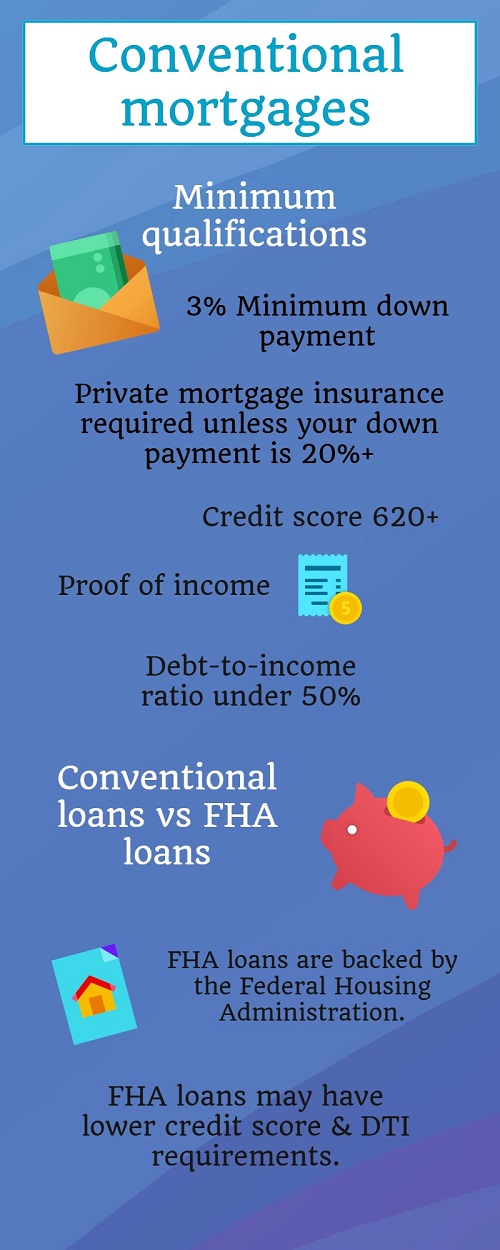

A down payment is required for conventional loans. Each lender has different minimum requirements, but the larger the down payment, the less money you’ll have to pay back over time.

Many believe a 20% down payment is required for conventional loans, but the minimum requirement is typically much lower. You can find mortgages with minimum down payment requirements anywhere from 3% to 20% of the overall purchase price.

Your choice of down payment amount can affect the terms of your mortgage, like interest rate or the need for private mortgage insurance.

Government-backed home loans have specific features to suit some homebuyers.

The Federal Housing Administration (FHA) is a government institution offering home loans for buyers who meet certain qualifications. Government-backed loans have advantages for those with bad credit or other financial roadblocks, but require other qualifications for approval.

Conventional mortgages tend to have higher interest rates than FHA loans, although these loans typically require borrowers to pay mortgage-insurance premiums.

Interest rates charged on a conventional mortgage vary by several factors, including the term and amount borrowed. However, interest rates are also subject to change every year based on the overall economy. Many buyers choose to wait for a period when interest rates are lower to apply for a mortgage, regardless of the loan type.

Ultimately, your choice of loan will depend on your personal circumstances. The more you know about different types of mortgage, the better equipped you’ll be for your journey into thefinancial real estate marketplace.

I have been selling Real Estate in the Greater Boston Area since 1997. I am the Co-Founder & Current Broker/Owner of Realty Executives in Watertown. A lifelong resident of Watertown which I still reside with my Wife Debra and my Twins Emily & Christopher. I am a supporter of many local & national charities. One of my most rewarding fundraisers was as a rider in the PanMass Challenge in 2010,2011,2015 & 2016 raising over $50,000 over those 4 years for the Dana Farber Jimmy Fund. I am a 1988 Graduate of Bentley University in Waltham. I have extensive knowledge of all types of Real Estate participating in over 1000 transactions. I also have New Construction experience & specialize in condo conversions.

Purchasing a home is one of the single most important investments in a person's life. With my expertise and guidance in the home buying and selling process, I can help find the most appropriate home for you. You can be assured that an experienced Real Estate Professional is working with your interests in mind. Please contact me on my cell at 617-799-8948 or email [email protected] for a free consult if you are thinking of Buying or Selling your home.